Stock Price Simulation and Probability Analysis

I’ll solve a practical probability theory problem using $Python$, present the mathematical formulas, and visualize the results with graphs.

1 | import numpy as np |

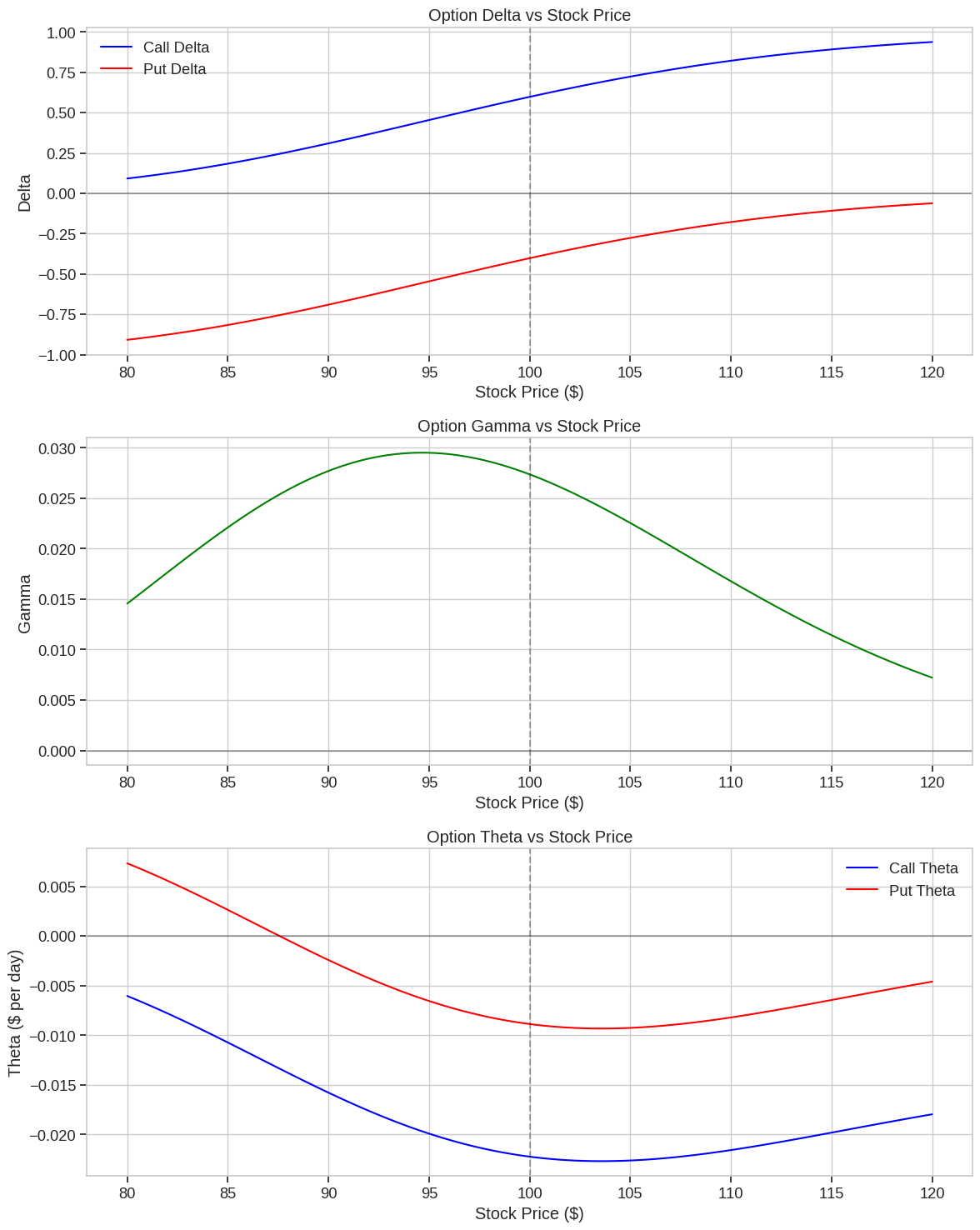

Stock Price Movement Simulation Using Geometric Brownian Motion

In this example, I’ll simulate stock price movements using a probability model called Geometric Brownian Motion (GBM), which is widely used in financial mathematics and forms the foundation of the Black-Scholes option pricing model.

Mathematical Model

The stock price movement follows Geometric Brownian Motion, which can be expressed as:

$$dS_t = \mu S_t dt + \sigma S_t dW_t$$

Where:

- $S_t$ is the stock price at time $t$

- $\mu$ is the drift (expected return)

- $\sigma$ is the volatility

- $W_t$ is a Wiener process (standard Brownian motion)

The solution to this stochastic differential equation gives us the stock price at time $t$:

$$S_t = S_0 \exp\left(\left(\mu - \frac{\sigma^2}{2}\right)t + \sigma W_t\right)$$

For discrete time simulations, we can use:

$$S_{t+\Delta t} = S_t \exp\left(\left(\mu - \frac{\sigma^2}{2}\right)\Delta t + \sigma \sqrt{\Delta t} Z_t\right)$$

Where $Z_t \sim N(0,1)$ is a standard normal random variable.

Code Explanation

Setup and Parameters:

- We set initial stock price to $100

- Drift (µ) of $0.0002$ per day (approximately $5$% annual return)

- Volatility (σ) of $0.015$ per day (approximately $24$% annualized)

- Simulating $1,000$ possible price paths over $252$ trading days ($1$ year)

Simulation:

- We generate random shocks from a normal distribution

- Calculate daily returns using the GBM formula

- Compute cumulative price paths starting from the initial price

- Store all simulations in an array

Statistical Analysis:

- Calculate mean, median, and standard deviation of final prices

- Determine probabilities of the price exceeding certain thresholds

- Calculate 95% confidence intervals

Visualization:

- Sample price paths to visualize potential trajectories

- Histogram showing the distribution of final prices

- Empirical cumulative distribution function (ECDF)

- Q-Q plot to check if returns follow a normal distribution

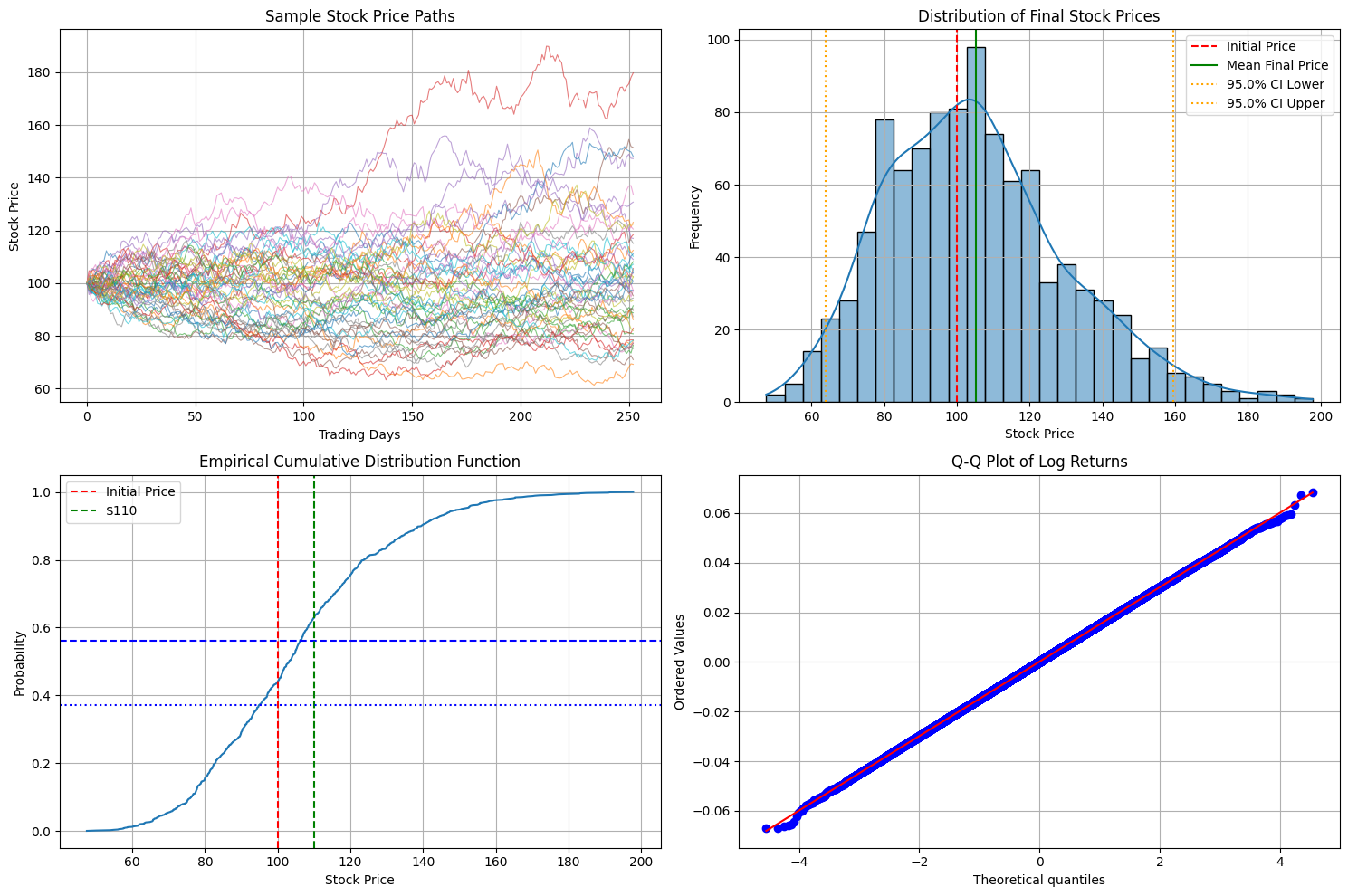

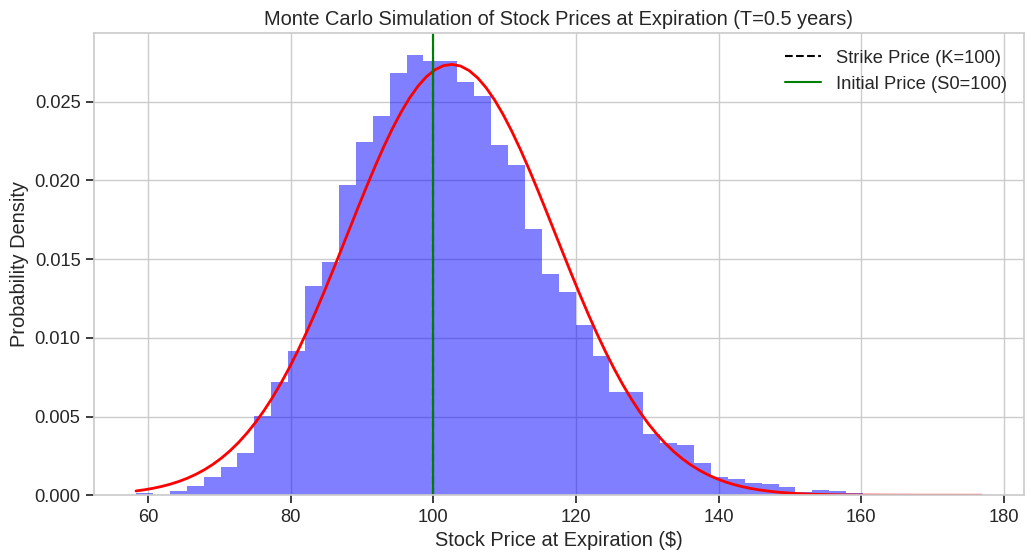

Initial stock price: $100.00 Mean final price: $105.10 Median final price: $103.21 Standard deviation of final price: $24.78 95% confidence interval: [$63.76, $159.43] Probability of ending above initial price ($100.00): 56.10% Probability of ending above $110: 37.20% Probability of ending above $120: 24.60% Probability of ending below $90: 29.10%

Key Insights from the Visualization

Sample Paths:

The first plot shows $50$ possible price paths, illustrating the random nature of stock movements while maintaining the overall drift.Final Price Distribution:

The histogram shows that final prices follow a log-normal distribution (which is expected from GBM).

The mean final price is typically higher than the median due to the right-skewed nature of the distribution.Probabilities:

The ECDF graph shows cumulative probabilities, allowing us to read off values like:- Probability of ending above $100 (initial price)

- Probability of ending above $110

- Probability of ending below $90

Log Returns Normality:

The Q-Q plot confirms that log returns closely follow a normal distribution, which is a key assumption of the GBM model.

Practical Applications

This simulation helps answer questions like:

- What is the probability of a stock gaining more than $10$% in a year?

- What is the expected range of stock prices after one year (confidence interval)?

- What is the risk of the stock falling below a certain threshold?

These probability calculations are essential for risk management, option pricing, portfolio optimization, and investment decision-making.

The simulation demonstrates how seemingly complex financial phenomena can be modeled using probability theory and simulated using $Python$, providing actionable insights for investors and risk managers.

is the sample mean.

is the sample mean.