Practical Example in Data Science: Predicting House Prices Using Linear Regression

We will solve a common data science problem: predicting house prices based on features like square footage and number of bedrooms.

This showcases the application of linear regression, a fundamental machine learning algorithm.

Problem Statement

We aim to predict house prices $( Y )$ using two features:

- Square footage $( X_1 )$

- Number of bedrooms $( X_2 )$.

The relationship is assumed to be linear:

$$

\text{Price} = \beta_0 + \beta_1 \cdot \text{SquareFootage} + \beta_2 \cdot \text{Bedrooms} + \epsilon

$$

where $( \epsilon )$ is the error term.

Python Implementation

1 | import numpy as np |

Explanation of Code

Data Generation:

square_footageandbedroomssimulate the main features of a house.priceis calculated using a predefined linear relationship plus random noise for realism.

Linear Regression:

- Using

statsmodels.OLS, we estimate coefficients $( \beta_0 )$, $( \beta_1 )$, and $( \beta_2 )$.

- Using

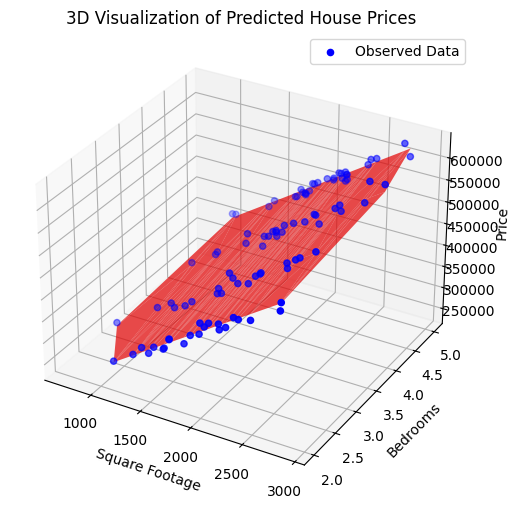

Visualization:

- A 3D scatter plot shows observed data points (blue dots).

- The red surface represents the predicted house prices based on the model.

Key Outputs

- Regression Summary:

- $Coefficients$: Show how house prices change with each feature.

- $R$-$squared$: Measures how well the model explains the variability in house prices.

OLS Regression Results

==============================================================================

Dep. Variable: Price R-squared: 0.984

Model: OLS Adj. R-squared: 0.984

Method: Least Squares F-statistic: 3049.

Date: Sun, 01 Dec 2024 Prob (F-statistic): 2.77e-88

Time: 03:00:00 Log-Likelihood: -1060.8

No. Observations: 100 AIC: 2128.

Df Residuals: 97 BIC: 2135.

Df Model: 2

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

const 4.882e+04 5331.911 9.157 0.000 3.82e+04 5.94e+04

SquareFootage 152.0480 2.201 69.074 0.000 147.679 156.417

Bedrooms 2.954e+04 868.797 33.999 0.000 2.78e+04 3.13e+04

==============================================================================

Omnibus: 7.854 Durbin-Watson: 2.034

Prob(Omnibus): 0.020 Jarque-Bera (JB): 8.131

Skew: 0.502 Prob(JB): 0.0172

Kurtosis: 3.971 Cond. No. 1.08e+04

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.08e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

- 3D Plot:

- The blue points are the actual data.

- The red plane shows the predicted relationship, helping to visualize the regression fit.

This example can be extended to include feature scaling, regularization (e.g., Ridge or Lasso regression), or additional predictors like location or age of the house.