Example Problem

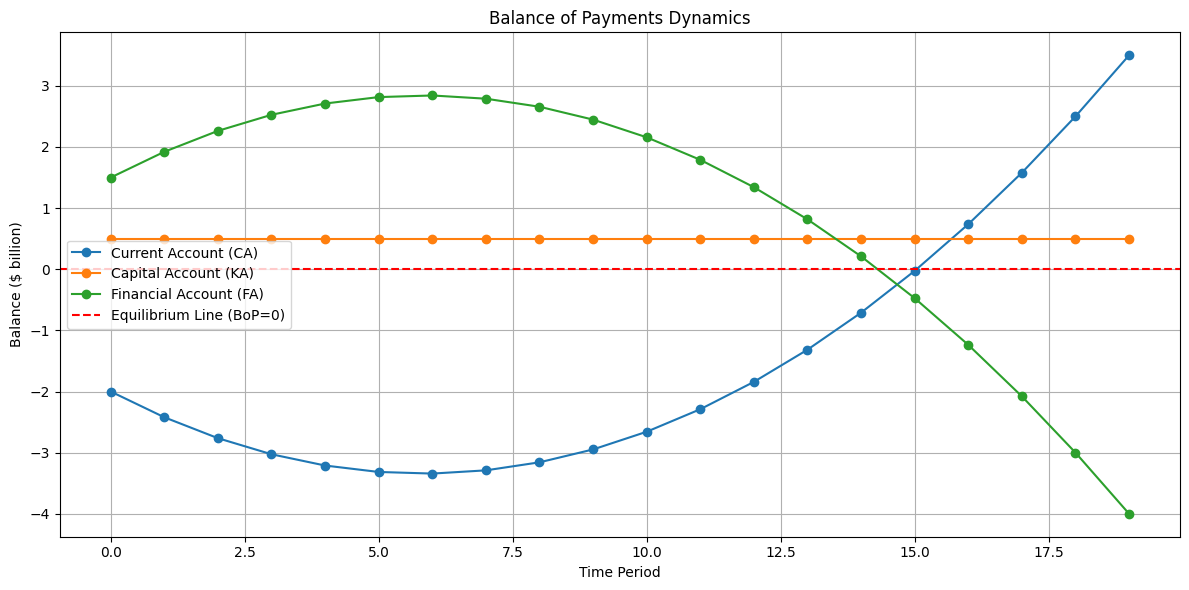

We aim to simulate a simplified BoP analysis to understand the interactions between the Current Account (CA), Capital Account (KA), and the Financial Account (FA).

Problem

- The Current Account (CA) records trade in goods and services, income, and transfers.

- The Capital Account (KA) reflects capital transfers and acquisition/disposal of non-produced assets.

- The Financial Account (FA) captures investments in financial assets.

By the BoP identity:

$$

\text{CA} + \text{KA} + \text{FA} = 0

$$

We will simulate and visualize:

- Changes in the CA due to trade balance adjustments.

- How these changes are offset by the KA and FA to maintain equilibrium.

Python Code

1 | import numpy as np |

Explanation

- Current Account Dynamics:

- Adjustments in trade balance affect the CA over time.

- BoP Equilibrium:

- The KA and FA adjust to ensure that the BoP identity $(\text{CA} + \text{KA} + \text{FA} = 0)$ holds.

- Assumptions:

- The KA remains constant for simplicity.

- Changes in the CA are offset entirely by the FA.

Results

- The graph shows how the Current Account evolves due to trade balance changes.

- The Financial Account responds dynamically to maintain BoP equilibrium.

- The Capital Account remains constant, highlighting its lesser role in this simplified example.

This example illustrates the balancing act within the BoP framework, showing the interdependence of its components.