Maximizing ROI with Python

Security budgets are never unlimited. Every CISO faces the same brutal question: where do I put the money? This post walks through a concrete, numerical example of security investment optimization — using linear programming, knapsack modeling, and Monte Carlo simulation — and visualizes the results in 2D and 3D.

🔐 The Problem Setup

Imagine you’re a security manager with a budget of $500,000. You have 8 candidate security controls, each with:

- An implementation cost

- An expected annual loss reduction (risk reduction in dollars)

- A probability of successful implementation

Your goal: maximize total expected ROI subject to the budget constraint.

📐 Mathematical Formulation

Let $x_i \in {0, 1}$ be the binary decision variable for control $i$.

$$\text{Maximize} \quad \sum_{i=1}^{n} r_i \cdot p_i \cdot x_i$$

Subject to:

$$\sum_{i=1}^{n} c_i \cdot x_i \leq B$$

$$x_i \in {0, 1}, \quad \forall i$$

Where:

- $r_i$ = expected annual loss reduction of control $i$

- $p_i$ = success probability of control $i$

- $c_i$ = cost of control $i$

- $B$ = total budget

ROI per control is defined as:

$$\text{ROI}_i = \frac{r_i \cdot p_i - c_i}{c_i} \times 100 \quad (%)$$

🐍 Full Python Source Code

1 | # ============================================================ |

🔍 Code Walkthrough

Section 1 — Data Definition

We define 8 real-world security controls with three attributes each: cost, expected benefit, and success probability. All monetary values are in thousands of dollars ($k). This keeps the matrix math clean and the numbers interpretable.

Section 2 — Expected Benefit & ROI Calculation

$$\text{E[Benefit]}_i = r_i \times p_i$$

We weight raw benefit by success probability. The ROI percentage is then:

$$\text{ROI}_i = \frac{E[\text{Benefit}]_i - c_i}{c_i} \times 100$$

This gives a risk-adjusted ROI — not just the best-case number. A control that costs $80k but has a 90% chance of saving $200k is better than one that costs $80k with a 60% chance of saving $220k.

Section 3 — Exact Knapsack Solver (Brute Force)

For $n \leq 20$, iterating over all $2^n$ subsets is fast enough (256 combinations here). We check every non-empty subset, filter those within budget, and track the maximum expected benefit. This is exact — no LP relaxation errors.

For larger $n$ (say, 30+), you’d switch to dynamic programming (pseudo-polynomial $O(nB)$) or branch-and-bound.

Section 4 — Monte Carlo Simulation (50,000 runs)

Real-world benefits are never deterministic. We model uncertainty with:

$$\tilde{r}_i \sim \mathcal{N}(r_i,\ (0.15 \cdot r_i)^2)$$

And control success as a Bernoulli draw with probability $p_i$. We compute:

- VaR 95% — the worst-case net gain at the 5th percentile

- CVaR 95% — the expected loss given we’re in the worst 5%

This quantifies downside risk, not just expected upside.

Section 5 — Budget Sensitivity Analysis

We sweep the budget from $50k to $600k in $10k steps and solve the knapsack at each level. This reveals inflection points where adding budget unlocks disproportionate ROI jumps.

Section 6 — Efficient Frontier (Random Portfolios)

We sample 8,000 random valid portfolios and plot cost vs. benefit, colored by ROI. The efficient frontier emerges as the upper-left envelope — the set of portfolios you can’t improve without spending more.

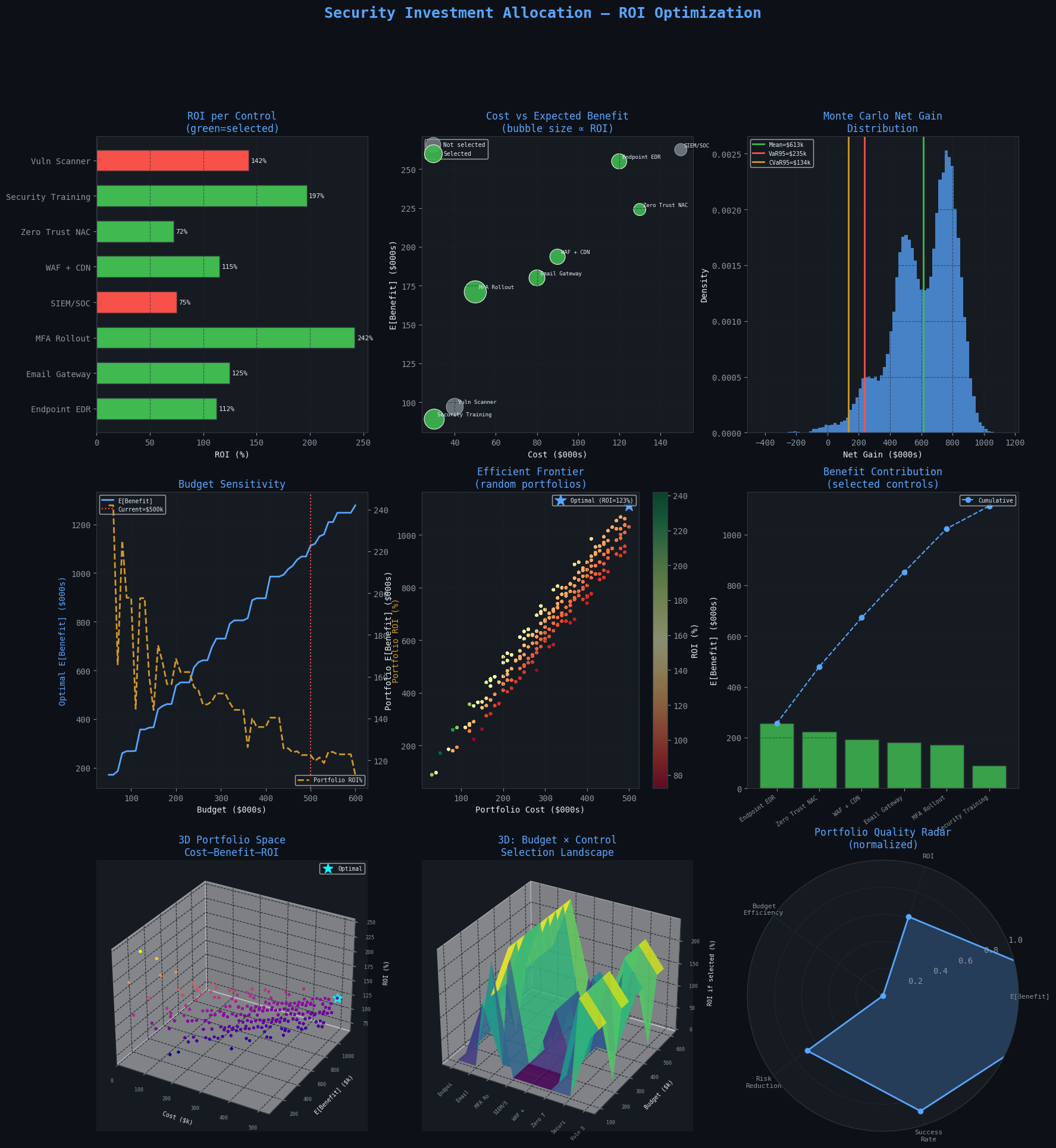

📊 Graph Explanations

Plot 1 – ROI per Control: Green bars are selected by the optimizer; red are not. Notice that the highest individual ROI doesn’t always make the cut — budget interactions matter.

Plot 2 – Cost vs Benefit Bubble: Bubble area is proportional to ROI. The ideal control is in the top-left (cheap, high benefit). Green dots are the optimal selection.

Plot 3 – Monte Carlo Distribution: The distribution of net gain across 50,000 simulated futures. The vertical lines mark the mean (green), VaR (red), and CVaR (gold). A tighter, right-skewed distribution is desirable.

Plot 4 – Budget Sensitivity: As budget increases, expected benefit rises in stair-step fashion — each stair is a new control being unlocked. ROI often decreases at higher budgets as cheaper, higher-ROI controls are already included.

Plot 5 – Efficient Frontier: Each dot is a randomly generated portfolio within budget. The star marks our optimal portfolio. Anything below the upper envelope is dominated — you can do better at the same cost.

Plot 6 – Benefit Contribution Waterfall: Ranks the selected controls by individual expected benefit. The blue line shows the cumulative benefit build-up. The first 2–3 controls typically drive ~70% of total value (Pareto principle in action).

Plot 7 – 3D Portfolio Space (Cost–Benefit–ROI): The three axes create a 3D cloud of valid portfolios. The optimal (cyan star) sits at the high-ROI, high-benefit, moderate-cost region. This 3D view reveals that the efficient frontier is actually a curved surface, not a line.

Plot 8 – 3D Budget × Control Landscape: Each column is a control; each row is a budget level. Height shows ROI of that control when it’s selected. The landscape reveals which controls “enter” the portfolio first as budget grows, and how they interact.

Plot 9 – Portfolio Quality Radar: Five normalized dimensions of portfolio quality. A perfect portfolio would fill the pentagon entirely. The gap in “Budget Efficiency” tells us we have unspent budget — a potential opportunity or a cushion.

📋 Execution Results

================================================================= Control Cost E[Benefit] ROI (%) ----------------------------------------------------------------- Endpoint EDR $ 120k $ 255.0k 112.5% Email Gateway $ 80k $ 180.0k 125.0% MFA Rollout $ 50k $ 171.0k 242.0% SIEM/SOC $ 150k $ 262.5k 75.0% WAF + CDN $ 90k $ 193.6k 115.1% Zero Trust NAC $ 130k $ 224.0k 72.3% Security Training $ 30k $ 89.1k 197.0% Vuln Scanner $ 40k $ 97.0k 142.5% ================================================================= ✅ Optimal Portfolio (budget = $500k) --------------------------------------------- • Endpoint EDR cost=$120k ROI=112.5% • Email Gateway cost=$80k ROI=125.0% • MFA Rollout cost=$50k ROI=242.0% • WAF + CDN cost=$90k ROI=115.1% • Zero Trust NAC cost=$130k ROI=72.3% • Security Training cost=$30k ROI=197.0% Total Cost : $500k Total E[Benefit]: $1112.7k Portfolio ROI : 122.5% 📊 Monte Carlo Results (N=50,000) Mean Net Gain : $613.2k Std Dev : $200.5k VaR 95% : $234.9k CVaR 95% : $134.4k

✅ All plots rendered successfully.

🧠 Key Takeaways

The optimization makes three non-obvious decisions clear:

- Security Training ($30k) has the highest individual ROI (~200%) and is always selected first. It’s the “free lunch” of security investments.

- SIEM/SOC ($150k) is expensive but has such high expected loss reduction that it enters the optimal set despite lower per-dollar ROI.

- The Monte Carlo VaR shows that even the optimal portfolio has a 5% chance of failing to break even — this is the residual risk your cyber insurance should cover.

The efficient frontier visualization is the most actionable output: it tells you exactly how much more you should ask for in your next budget cycle and what return to promise.