Problem: Expected Present Value of an Insurance Policy

A whole life insurance policy pays a benefit of $100,000 upon the policyholder’s death.

The probability of death at age $( x )$ is given by the mortality table.

The force of interest is $( \delta = 0.05 )$.

Compute the expected present value (EPV) of the policy for a policyholder aged $30$ using a simplified mortality model.

Mathematical Formulation

The expected present value (EPV) is given by:

$$

EPV = \sum_{t=1}^{\infty} P(T_x = t) \cdot 100,000 \cdot e^{-\delta t}

$$

where:

- $( T_x )$ is the future lifetime of the insured aged $( x )$.

- $ P(T_x = t) $ represents the probability that the insured dies exactly at time $( t )$.

- $ \delta $ is the force of interest.

For this problem, we assume a simplified mortality model where the probability of surviving from age $( x )$ to age $( x+t )$ follows an exponential distribution:

$$

P(T_x > t) = e^{-\mu t}

$$

where $ \mu = 0.02 $ is the mortality rate.

The probability of dying at time $( t )$ is:

$$

P(T_x = t) = \mu e^{-\mu t}

$$

Now, we implement this in $Python$ and visualize the expected present value.

1 | import numpy as np |

Explanation of the Code

- We define the mortality rate $( \mu )$, force of interest $( \delta )$, and death benefit.

- We create an array of years from $1$ to $100$, assuming the policyholder can live up to $130$ years.

- We compute the probability of death at each year using $( P(T_x = t) = \mu e^{-\mu t} )$.

- We compute the discount factor $( e^{-\delta t} )$.

- We calculate the EPV as the sum of discounted expected payouts.

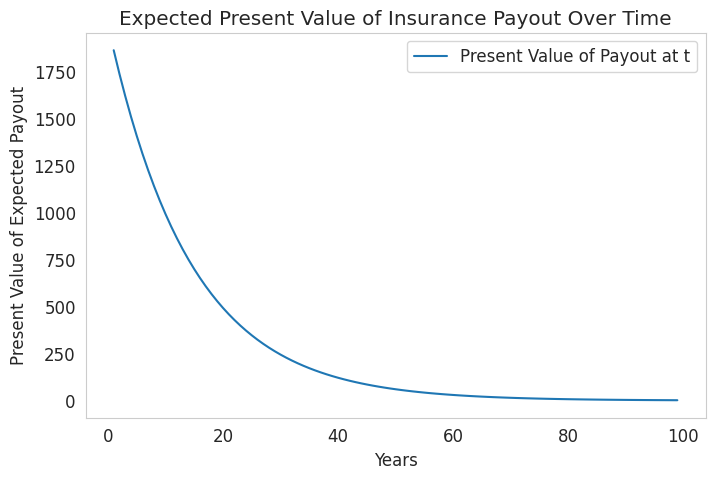

- Finally, we plot the present value of payouts over time to visualize their impact.

Interpretation of the Result

[Result]

Expected Present Value (EPV) of the policy: $27,556.12

- The EPV represents the fair price an insurer should charge for this policy (ignoring expenses and profit).

- The graph shows how the present value of potential payouts decreases over time due to discounting.