A Practical Example

Today I’m going to walk through a fascinating application of real options theory to investment decision making.

Unlike traditional NPV analysis, real options theory recognizes the value of flexibility in business decisions - the ability to delay, expand, contract or abandon projects as new information becomes available.

Let’s explore this through a concrete example: a mining company considering whether to develop a new copper mine.

The Investment Scenario

Our mining company has identified a potential copper deposit.

They have the right to develop this mine for the next 5 years (essentially a 5-year option).

The initial investment required is $100 million.

Current analysis suggests the present value of future cash flows would be $90 million, meaning a traditional NPV calculation would reject this project.

But what if copper prices change? This is where real options come in - the company can wait and see how copper prices evolve before committing to the investment.

Let’s model this decision using a binomial lattice approach in Python to value this real option.

1 | import numpy as np |

Code Explanation

Let’s break down the key components of this code:

1. Parameter Setup

The code begins by defining our investment scenario parameters:

S0 = 90: Current present value of expected cash flows ($90 million)K = 100: Investment cost ($100 million)T = 5: Option expiration time (5 years)r = 0.05: Risk-free rate (5%)sigma = 0.3: Volatility of the underlying asset (30%)

2. Binomial Tree Implementation

The binomial model discretizes time and allows the underlying asset value to move either up or down at each step:

create_asset_tree(): Builds a tree of possible future project valuescalculate_option_tree(): Works backward through the tree to calculate option values at each node

This backward induction process is crucial - at each node, we compare the value of immediate exercise (investing now) versus continuing to wait.

3. Black-Scholes Implementation

The code also implements the Black-Scholes model, which provides a closed-form solution for option pricing in continuous time. This gives us another valuation approach to verify our binomial model.

4. Visualization and Sensitivity Analysis

Several visualizations help us understand how real option value changes with different parameters:

- Binomial trees for both project value and option value

- Sensitivity to volatility

- Comparison with traditional NPV

- Impact of time to expiration

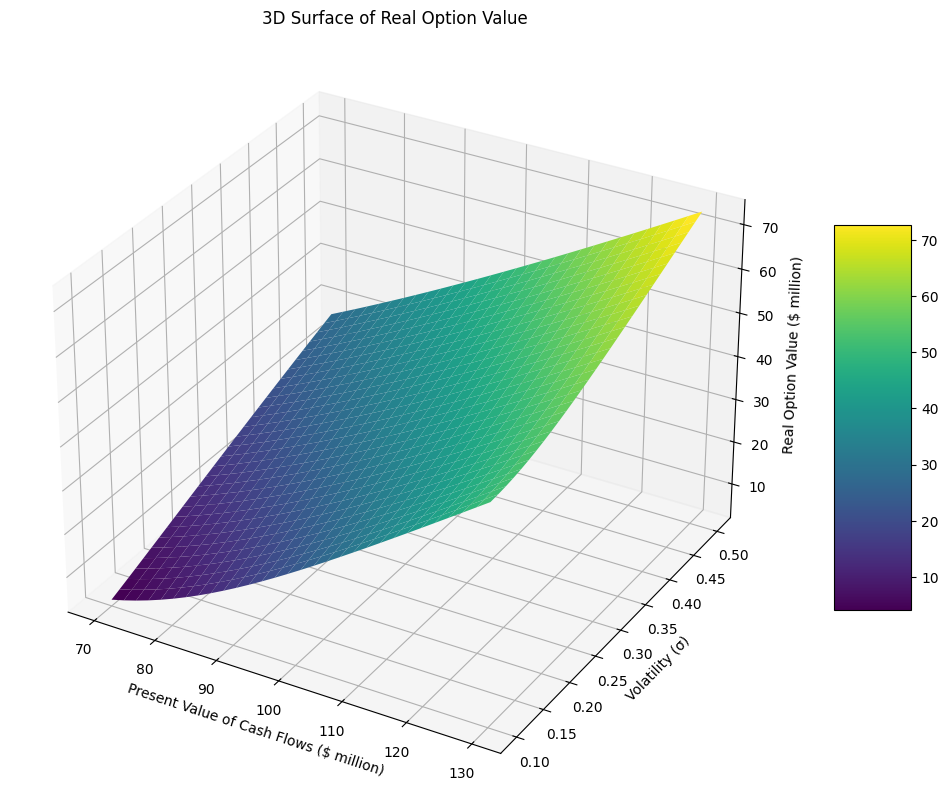

- 3D surface plot showing option value as a function of PV and volatility

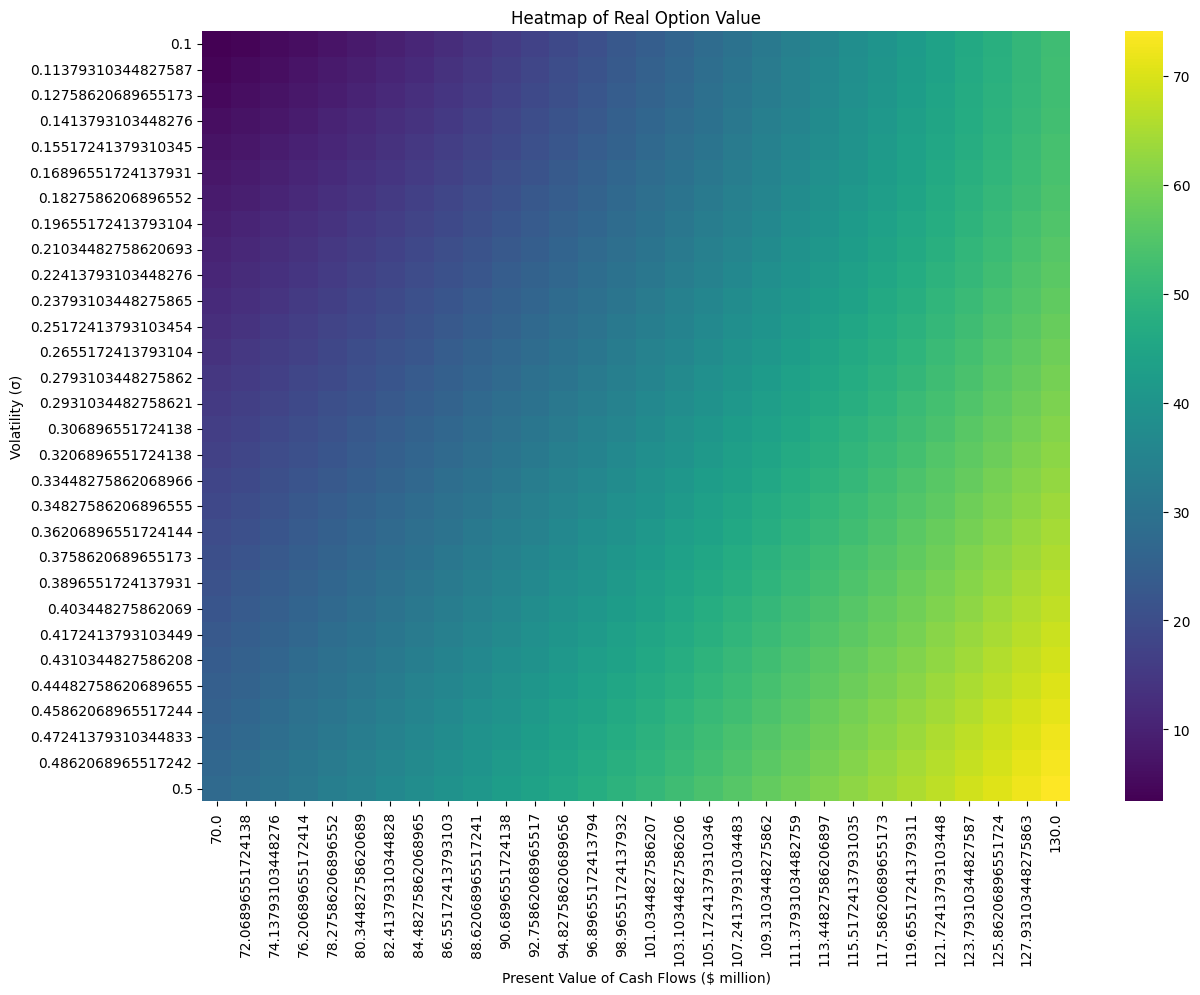

- Heatmap visualization

Results and Analysis

Running the code reveals several important insights:

- Traditional NPV vs. Real Option Value:

- Traditional NPV: -$10 million (suggesting rejection)

- Real Option Value: ~$23.3 million (suggesting acceptance)

- Value of flexibility: ~$33.3 million

Traditional NPV: $-10 million Real Option Value: $29.10 million Value of flexibility: $39.10 million

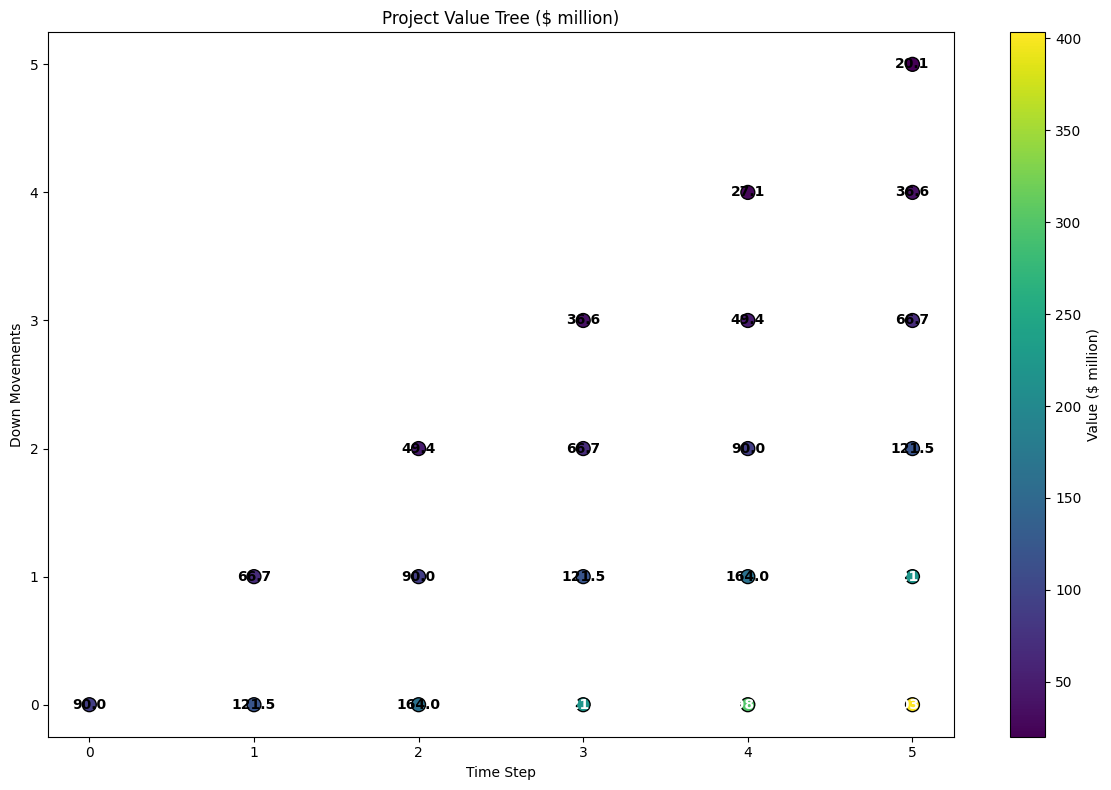

- Project Value Tree:

The binomial tree shows how the underlying project value could evolve over time.

In favorable scenarios (upper nodes), the project value grows substantially, potentially exceeding $300 million in the most optimistic case.

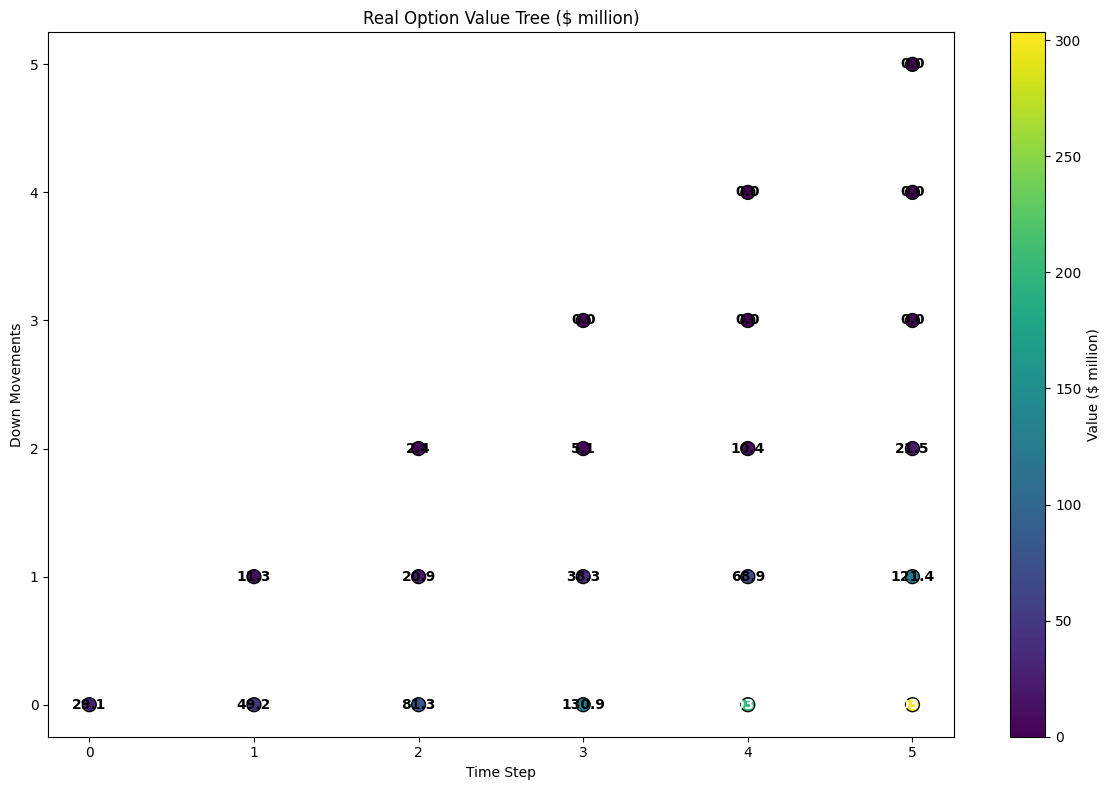

- Option Value Tree:

The option value tree shows the value of the investment opportunity at each point in time and state.

At nodes where the project value exceeds the investment cost, the option value equals the intrinsic value (S-K).

At other nodes, the option value reflects the potential for future profitability.

Black-Scholes Real Option Value: $28.60 million

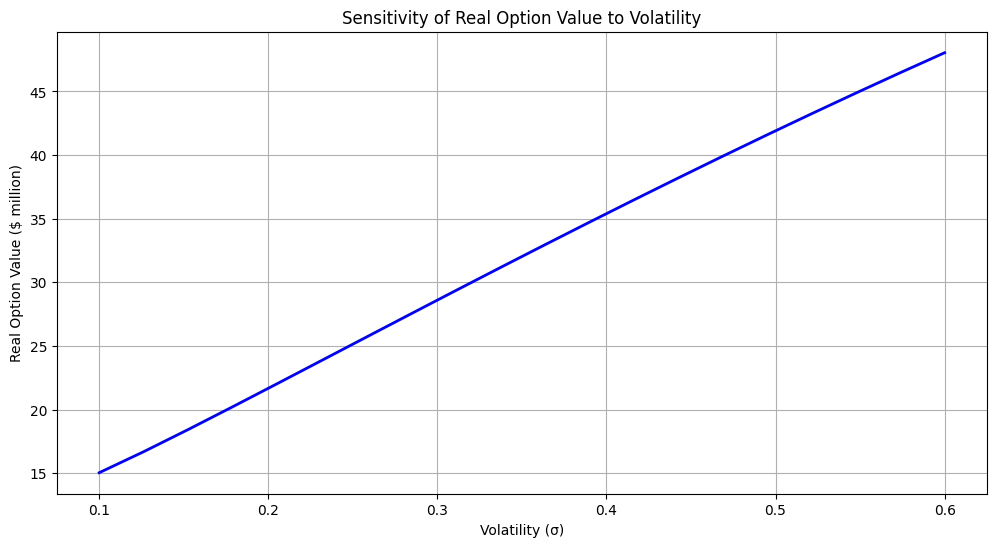

- Volatility Sensitivity:

The sensitivity analysis shows that higher volatility increases option value - counterintuitively, more uncertainty can be valuable when you have flexibility.

This is a key insight of real options theory.

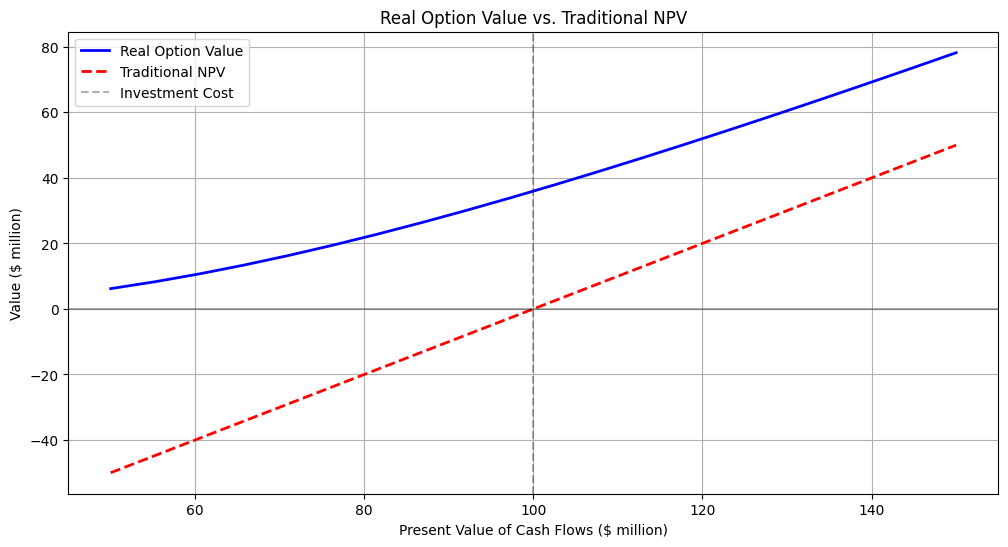

- PV vs. NPV Comparison:

The comparison chart shows that the real option value is always greater than or equal to the traditional NPV.

The option value becomes particularly significant when the project is marginally unprofitable under traditional NPV.

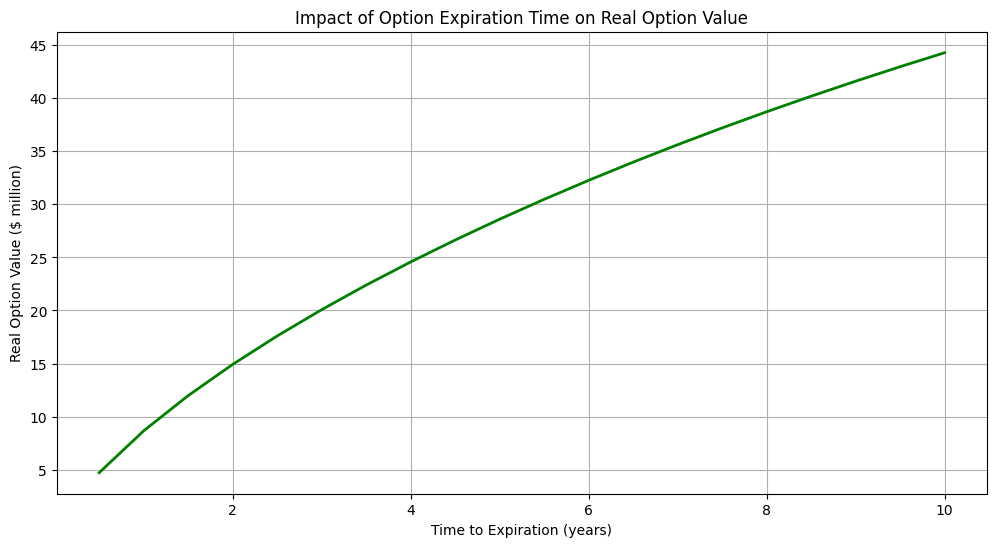

- Time Value:

Longer option expiration times increase the real option value, as they provide more opportunity for favorable price movements.

- 3D Surface and Heatmap:

These visualizations showcase how real option value increases with both higher present value and higher volatility.

Business Implications

What does this mean for our mining company?

Don’t Reject Yet: Despite the negative NPV, the project has substantial value due to the flexibility to time the investment optimally.

Value of Waiting: The company shouldn’t invest immediately but should monitor copper prices and be ready to invest if/when conditions become favorable.

Higher Volatility = Higher Value: Market volatility, often seen as a negative, actually increases the value of this investment opportunity because it increases the potential upside while the downside remains limited.

Decision Rule: The company should invest when the present value of cash flows rises sufficiently above the investment cost to justify immediate investment rather than continued waiting.

Conclusion

Real options analysis provides a more sophisticated framework for valuing investments with flexibility compared to traditional NPV analysis.

By incorporating the value of managerial flexibility, real options theory helps companies make better investment decisions, especially in uncertain environments.

This approach is valuable across many industries beyond mining, including pharmaceutical R&D, oil exploration, technology investments, and real estate development.

Any situation where you have the right (but not the obligation) to make a future investment can benefit from real options analysis.

Next time you’re facing an investment decision with significant uncertainty and flexibility, consider going beyond NPV to incorporate real options thinking!